Executive Summary:

In March 2025, TechPro Systems, Inc., a SaaS provider, experienced a catastrophic fire at its primary data center. The incident caused extended service outages, significant operational downtime, and the loss of several key clients. Lakelet Advisory Group, LLC was retained to assess and quantify the resulting economic damages, including lost profits, client attrition, and associated mitigation costs. Following a detailed financial analysis, our team concluded that the total damages sustained amounted to approximately $16.2 million.

Background:

The fire resulted in a 17-day full outage, followed by 45 days of partial operations. The company lost key clients and experienced reputational damage, leading to the abandonment of $4.8 million in new contracts.

Scope of Engagement:

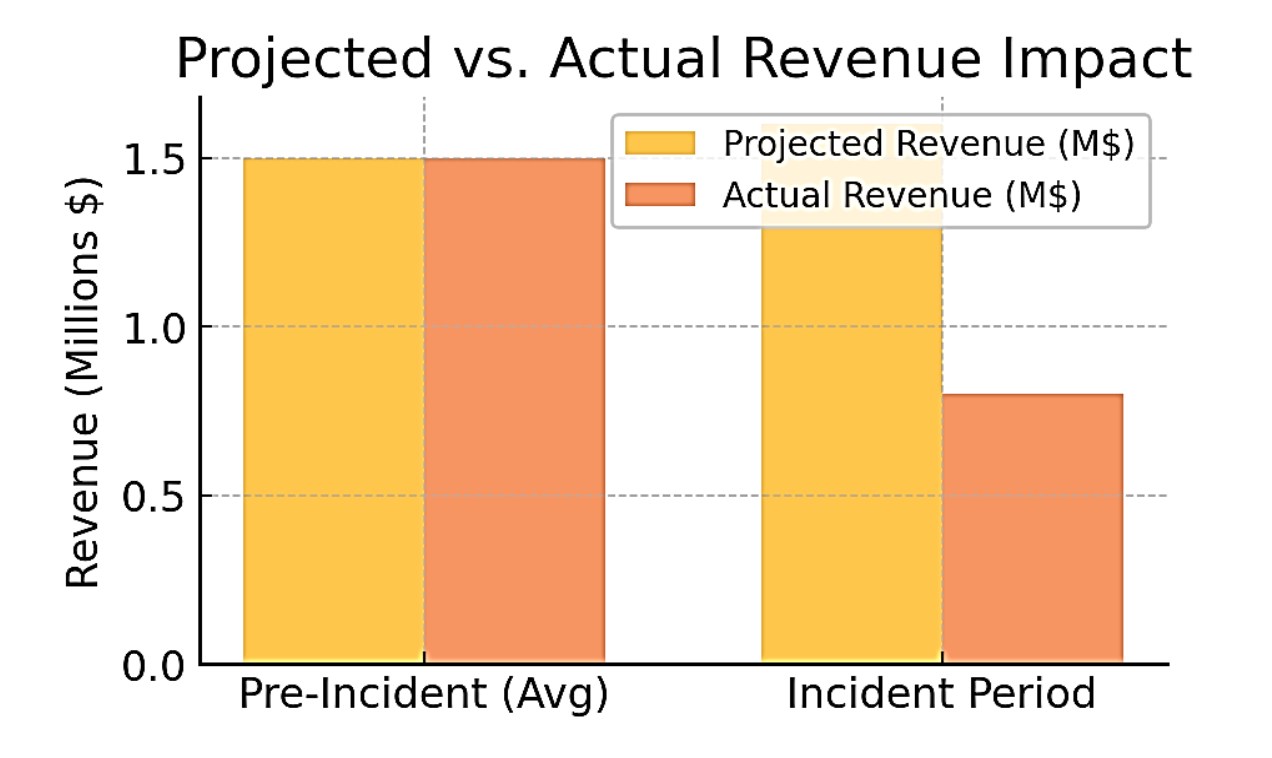

TechPro Systems, Inc. endured a prolonged operational disruption following the data center fire, with 17 days of complete outage and an additional 45 days of limited-service capacity. The prolonged instability resulted in approximately 15% client attrition, significantly impacting recurring revenue. Compounding the loss, the company forfeited $4.8 million in new business from abandoned contracts during the recovery period. In parallel, TechPro incurred $2.1 million in incremental expenses, including temporary server deployments, recovery operations, and customer compensation credits. Over a projected 12-month period, the cumulative impact of these disruptions led to an estimated $9.3 million in lost profits.

Key Methodologies:

But-for Financial Model using 2021–2023 performance as a baseline.

Customer Churn Analysis using historical churn data and client interviews.

Business Interruption Framework aligned with AICPA Practice Aid.

Discounting Future Losses using a 10% risk-adjusted discount rate.

Findings:

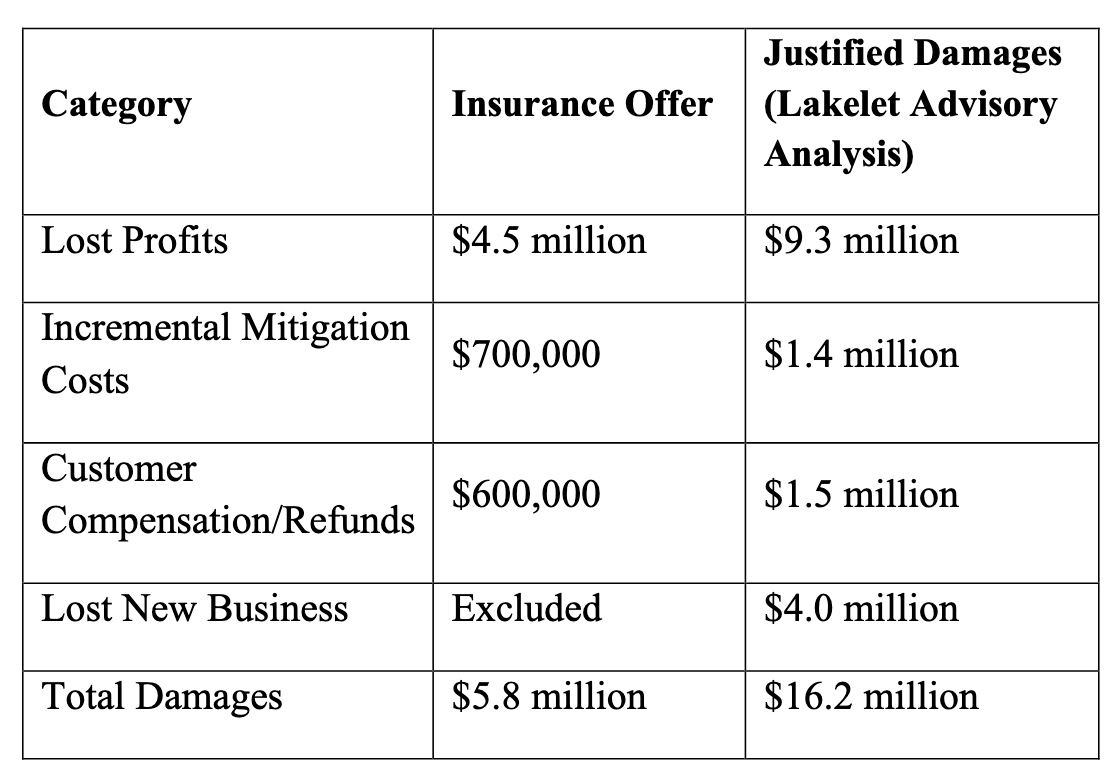

The total economic damages were quantified as follows:

Lost Profits: $9.3 million

Incremental Mitigation Costs: $1.4 million

Customer Compensation/Refunds: $1.5 million

Lost New Business: $4.0 million

Total Damages Quantified: $16.2 million

Outcome:

Our expert testimony supported the plaintiff’s claim, leading to a settlement of $13.6 million.

Exhibit 1: Projected vs. Actual Revenue:

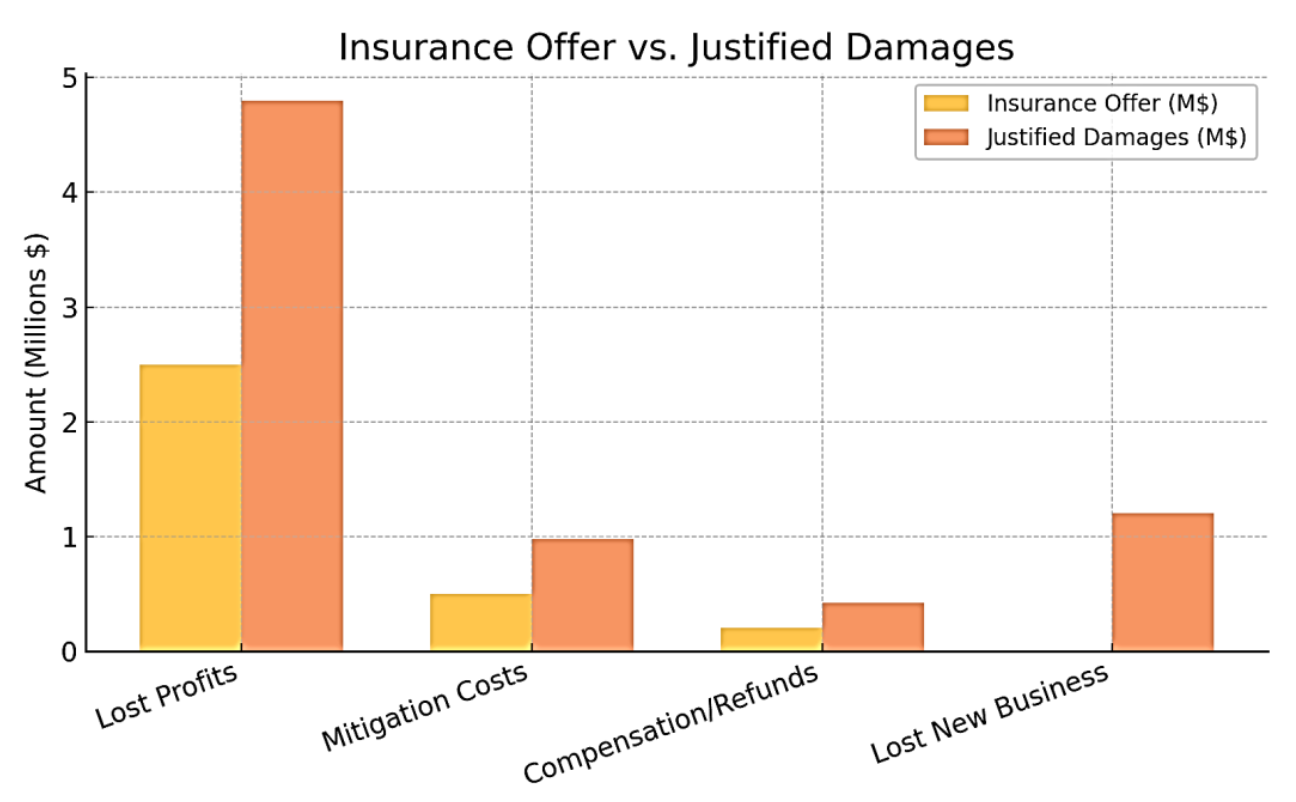

Insurance Offer vs. Justified Damages:

As part of the litigation process, TechPro Systems, Inc. filed a business interruption and property damage claim with its insurance provider. The initial insurance settlement offer was deemed insufficient compared to the true economic impact of the disaster. Our analysis provided a detailed rebuttal with substantiated financial modeling, leading to a favorable settlement.

Our evidence-based analysis nearly tripled the recognized damages from the insurance provider’s initial offer. This detailed quantification of downtime, client attrition, and lost future contracts proved essential in negotiating the final settlement.

Exhibit 2: Insurance Offer vs. Justified Damages:

Final Settlement Outcome:

After arbitration, the company received approximately 84% of the damages quantified by Lakelet Advisory Group, resulting in a final recovery of approximately $13.6 million (84% of $16.2 million).

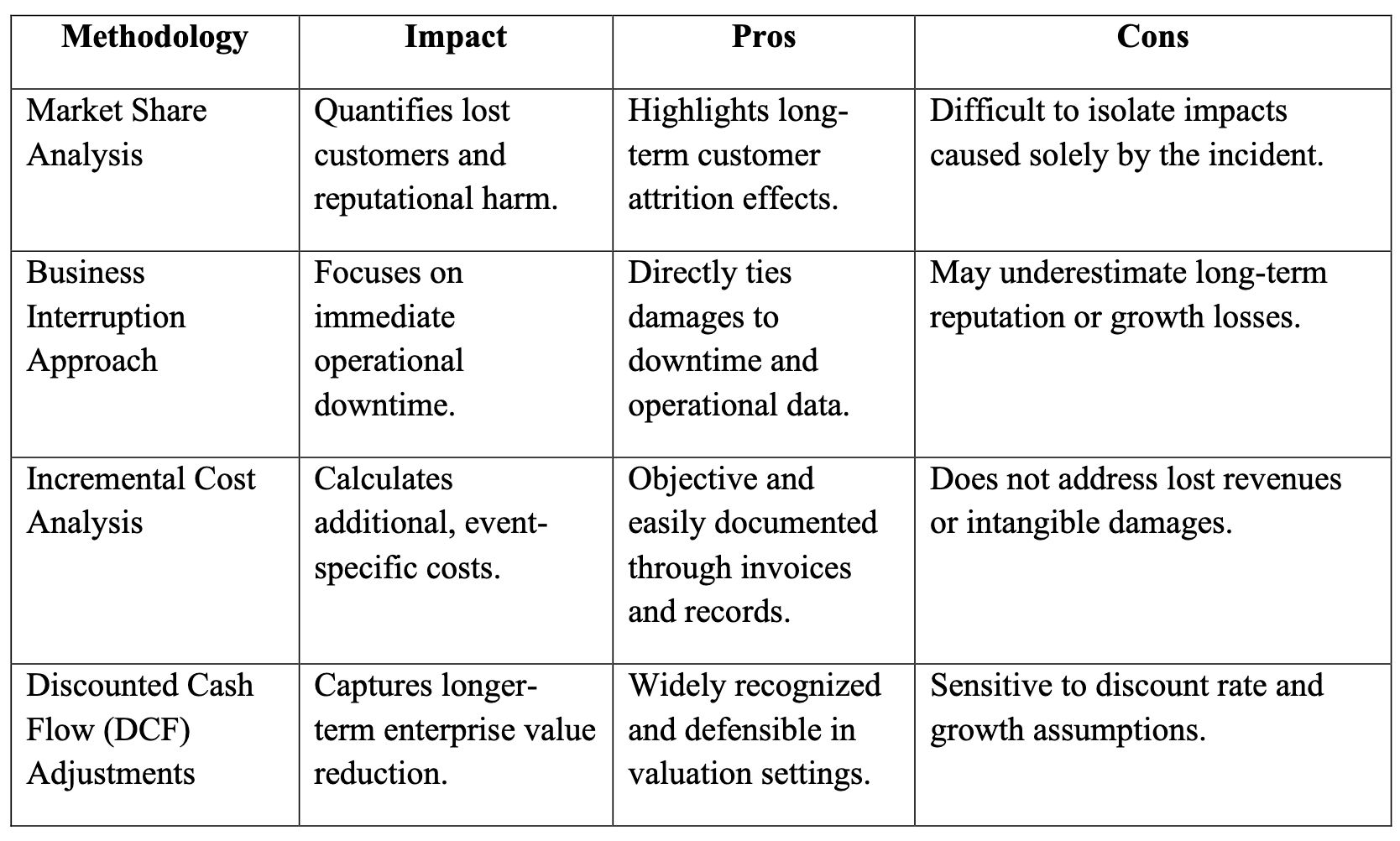

Economic Loss Methodologies Utilized:

The following economic loss methodologies were considered and could have been utilized to quantifydamages resulting from the disaster:

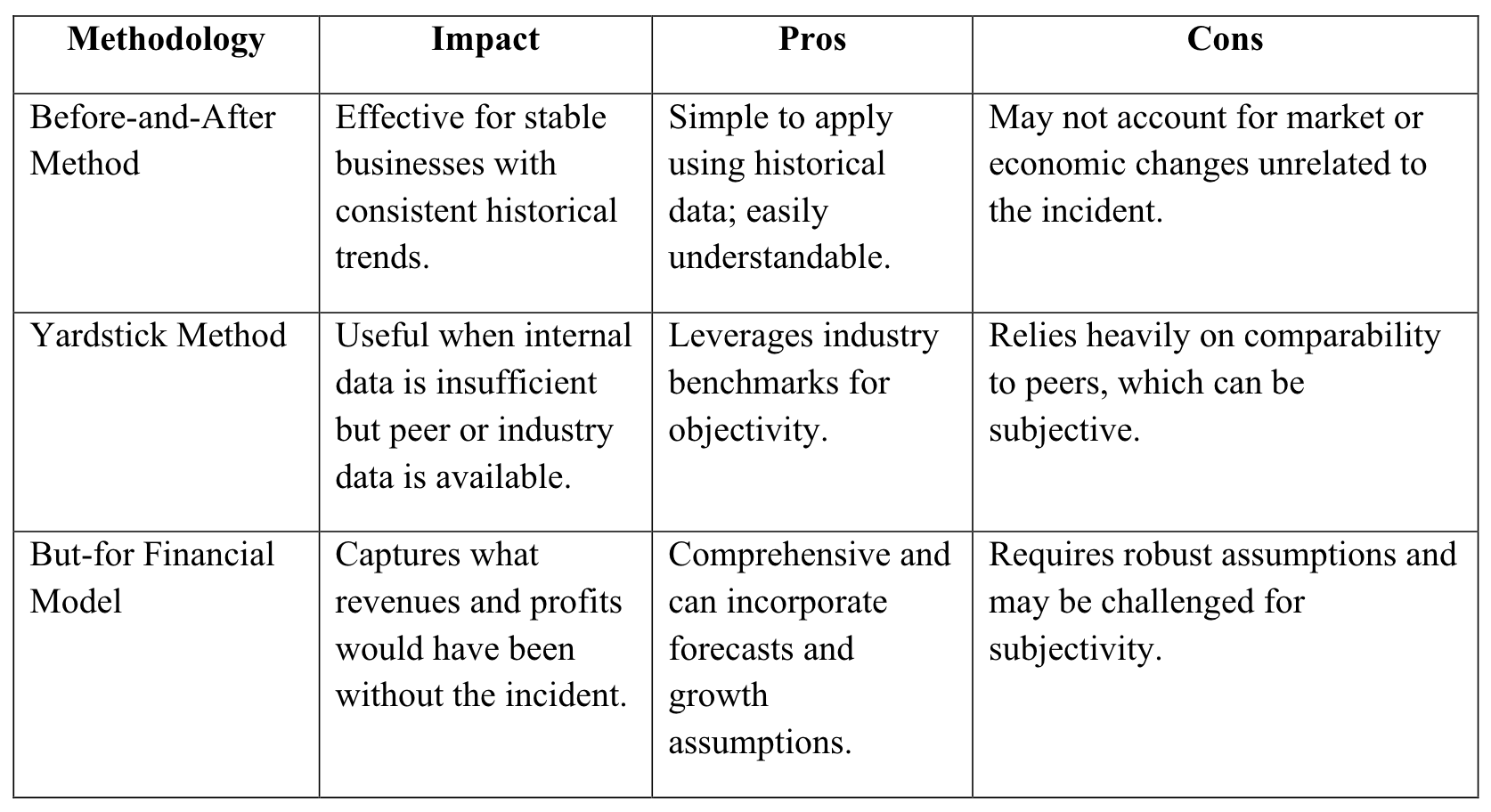

Before-and-After Method – Compares the company’s actual performance post-event to its historical performance prior to the incident, isolating the financial impact of the disruption.

Yardstick Method – Uses comparable companies or industry benchmarks to estimate what the company’s performance would have been but for the incident.

But-for Financial Model – Constructs a projection of revenue and profits assuming the event had not occurred, and contrasts this with actual results to determine lost profits.

Market Share Analysis – Evaluates lost customers or market share due to reputational harm and quantifies the future revenue impact over the recovery period.

Business Interruption Approach – Estimates the period of full and partial operational downtime and applies margins to calculate lost income during that period.

Incremental Cost Analysis – Quantifies additional costs incurred for mitigation, temporary services, or client retention that would not have been incurred otherwise.

Discounted Cash Flow (DCF) Adjustments – Applies discounted cash flow techniques to quantify longer-term losses or reduced enterprise value due to the incident.

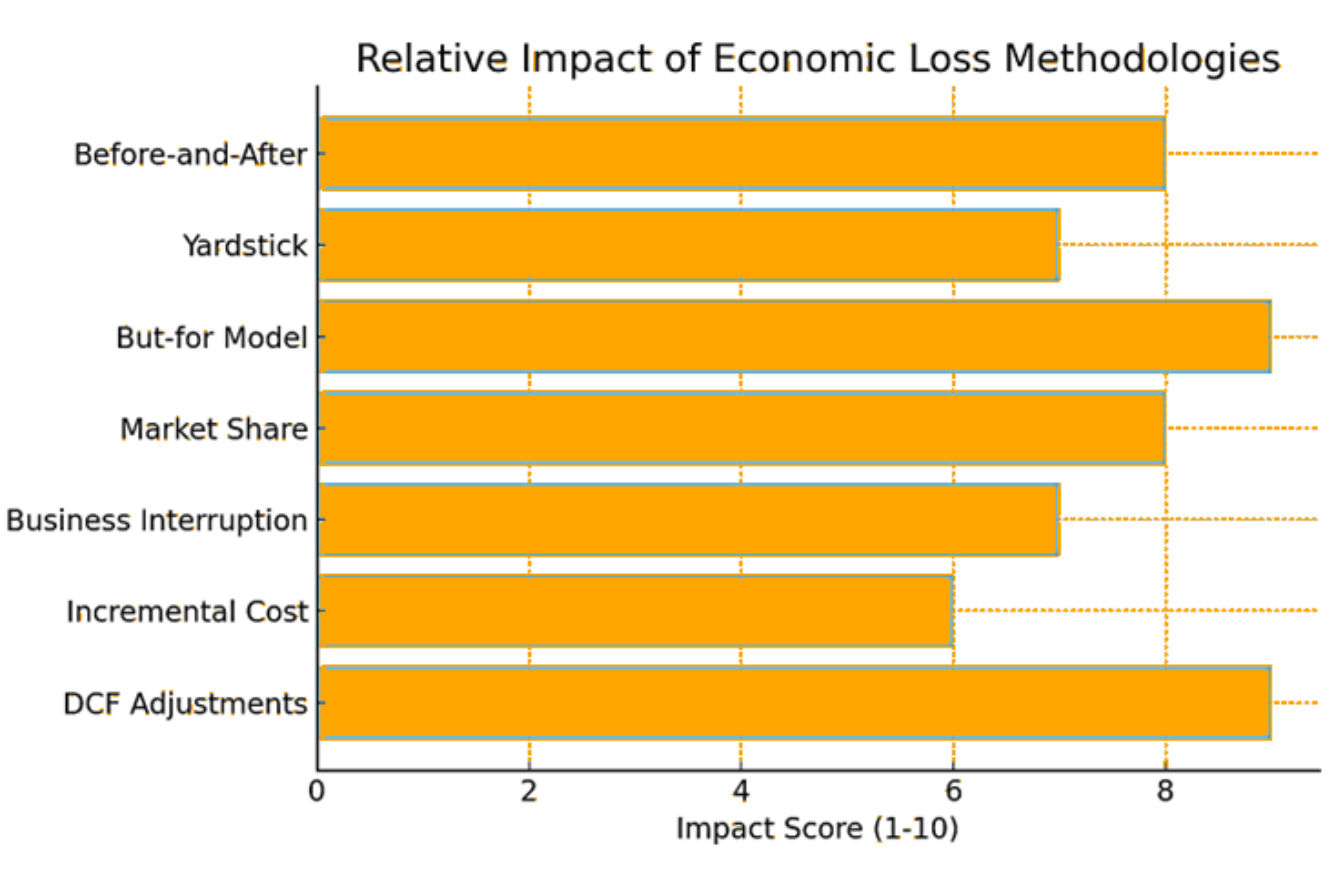

Methodology Impact Analysis:

The table below summarizes the potential impact of each economic loss methodology, along with its key pros and cons.

Exhibit 3: Impact of Economic Loss Methodologies:

Conclusion:

The But-for Financial Model and Discounted Cash Flow (DCF) Adjustments proved to be the most impactful methodologies in substantiating the claim and reaching a favorable settlement. These approaches effectively quantified both the immediate loss of profits and the longer-term effects on enterprise value. By incorporating client attrition and business interruption data, the analysis delivered a comprehensive assessment of both short-term disruptions and lasting financial harm. Ultimately, this integrated, multi-method strategy—underpinned by robust financial modeling—enabled the company to recover 84% of the total quantified damages, amounting to $13.6 million out of $16.2 million. This outcome underscores the critical importance of leveraging a tailored combination of loss quantification techniques, aligned with the unique circumstances of each case.