Background

As tax professionals, the ability to provide our clients with a “do over” as it pertains to their tax obligation can be one of the most helpful tools that can be provided. Obviously, this forgiveness or restructuring of one’s tax obligation requires the tax professional and their client to confront a litany of hurdles.

The Offer in Compromise (“OIC”) program was created by the IRS to allow taxpayers to settle their outstanding debt with the IRS for a lower, agreed-upon amount than what was originally owed. The idea behind the program is that many taxpayers cannot pay their tax liability without creating a significant financial hardship. The burden of proof to demonstrate one’s inability to meet their tax obligations rests on the taxpayer. Perhaps more so in this area where the taxpayer is seeking forgiveness or a restructuring on the tax obligation. To obtain this forgiveness, the IRS wants to know why you believe you will not be able to pay off the entire balance - the IRS isn’t going to take just any reason. Justification for the OIC does not include a recession, loss of a client, or poor record keeping. Nevertheless, the IRS has considered disability, substance abuse problems, huge balance amounts, dependent care, limited income potential as a result of advanced age, or serious health matters as good reasons. On average, over the past few years, the IRS accepted approximately $200,000,000 per year in OIC.

The acceptance of the OIC generally can be classified within three domains, these being:

Doubt as to liability. A taxpayer meets this requirement only if an effective difference as to the existence or amount due by the taxpayer

Doubt as to collectability exists. For example, where the taxpayer’s assets and income are less than the full amount of the tax liability. This is especially germane with distressed entities

Despite there being no doubt that the tax obligation exists, and the obligation amounts are known, and OIC may be accepted if by compelling said payment (in full as current required before the OIC) would either create a significant economic hardship or would be unfair and inequitable because of extraordinary conditions.

Obviously, many taxpayers may wish to have their tax obligations “erased or restructured.” However, it is a challenging process that requires justification, time, the experience of the right tax professionals, determining the amount that can be paid within the agreed upon time, and solid validation for the OIC amount. On average the OIC process, excluding appeals, has taken 4 – 6 months. Many of your clients will want to opt for the OIC route simply because it is the only option that lowers the total value of the tax owed. It is also for this reason that this method is the most advertised settlement option by tax resolution companies and accounting firms. The Latin adage is most appropriate - ‘Caveat Emptor’ (‘let the buyer beware’).

Probability of Obtaining an OIC and How to Increase that Opportunity

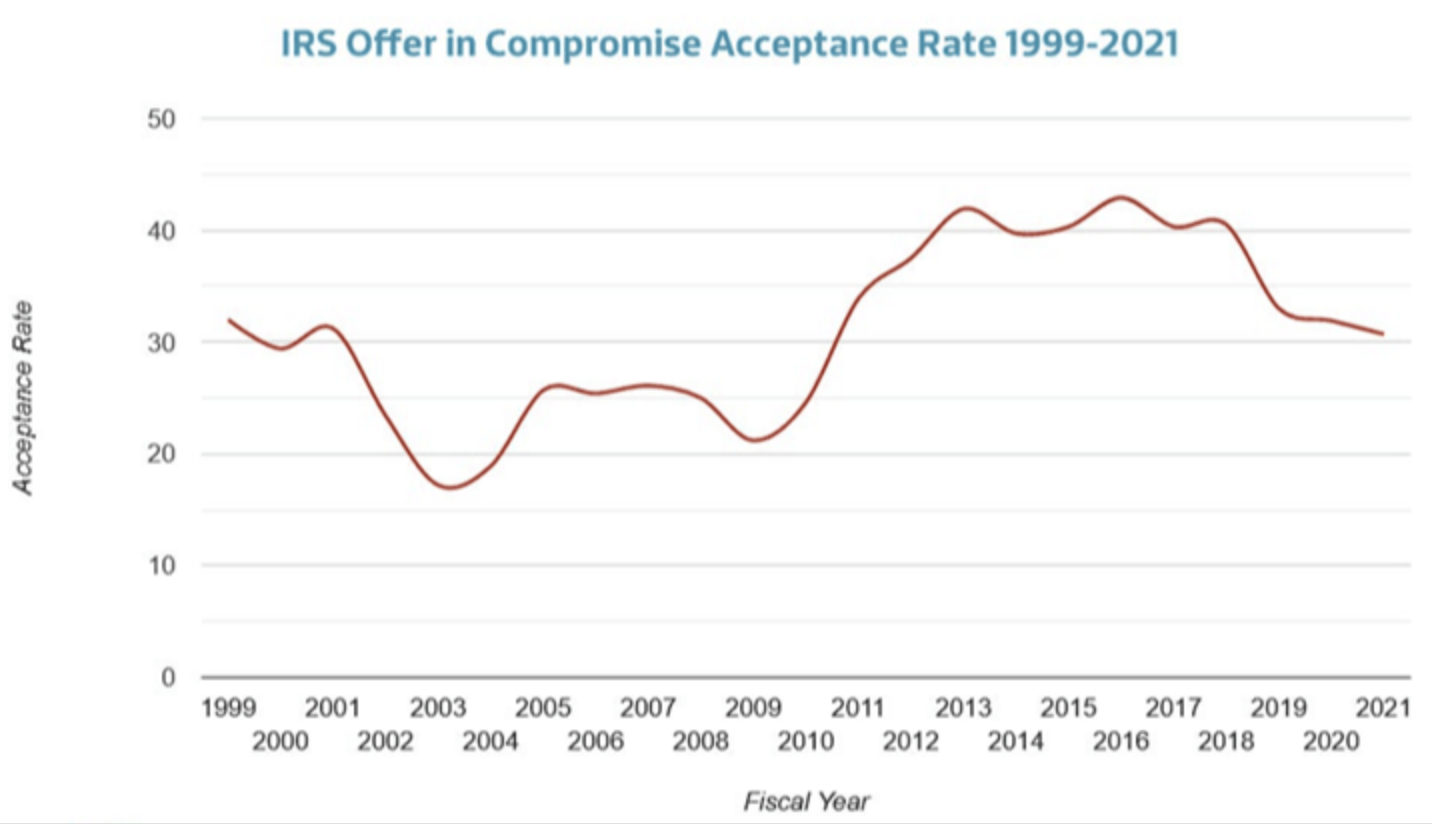

The role of the professional tax advisor is critical in the OIC process, perhaps more so than virtually any other area of negotiations or presentations with the IRS. Over the past few years, on average, only 30% of the OIC were accepted by the IRS. However, when the taxpayer works with a team of professionals, this acceptance rate has been increased by 70%. These statistics are based on the over 70,000 OIC applied for to the IRS. The following chart illustrates the increase in the number of OIC accepted by the IRS:

This article addresses how to geometrically improve our client’s probability of having the OIC accepted on terms which are fair to all parties. The opportunity for having a successful OIC, that is fair to all parties, is a function of several critical components. These being:

Communications

Accurate information

Professional prepared financial forecast/projections

Business Valuation.

Communications

With regards to the OIC, the tax professional needs to be candid with their client which includes, but is not limited to, managing their expectations as to the amounts, the costs of this process, and the timing. For example, even if the OIC is “awarded,” the taxpayer needs to understand that they will be under IRS scrutiny to ensure the assumptions made to derive the restructure amount have not been materially altered.

The candid communications are not only with your client but with the IRS. Eliminate any surprises – be frank, prompt, professional, and ensure the data provided is accurate and supportive. The most common mistakes are to apply for an OIC that is totally unrealistic (too low) and not supportable.

Accurate Information

This component to a successful OIC process may appear to be too obvious, even to the most novice reader. Too often the embarrassing situation is needing to amend the process due to new information. This not only forces the process to “restart,” but one loses credibility as to the over information, amounts and ability of the client to manage their financing.

Many of the taxpayers are in this very predicament because they do not have the basic financial controls in place and information available. More times than not the client will not have audited financial statements with reconciling schedules for all the transactions in question. The tax preparer must recreate the financial periods based upon limited data years after the events in question.

Spend the time and prepare a detailed set of documents with each applicable account/transaction reconciled and documented. For those areas that have gaps in support – document said gaps and advise the IRS representative accordingly.

Professional Prepared Financial Forecast/Projections

Before outlining the financial projections, allow me to summarize the importance of this process. The OIC is based upon the taxpayer’s ability to pay based upon the current economic environment and their future revenue stream(s). The preliminary amount that the IRS will pay is a function of two basic economic factors, these being:

What is the ability of the taxpayer to be able to pay over the next year or two? In other words, the financial projections of the taxpayer, PLUS:

The adjusted net value of their current economic situation. This will

be presented in more detail below.

A financial projection is a forecast of future revenues and expenses. Typically, the projection will account for internal or historical data and will include a prediction of external market factors. In general, you will need to develop both short- and mid-term financial projections. At a minimum, the financial projections should include:

A sales forecast, generally, for a three-year period

List all the associated expenses required to generate said sales

Identify and quantify all the Capital Expenditures required to support the revenue stream

Develop a cash-flow statement

Develop an Income Statement projections

Develop a Balance Sheet

Breakeven analysis

Use the historical financial results as a basis. Include the overall market and the results of your competitors. Document the differentiators associated with the taxpayer.

My recommendation to eliminate seasonality and provide comparability is to have the first three years monthly, summarized into quarterly and annual results. Detailed supporting document is a prerequisite for the OIC. OIC applicants are generally put through a demanding financial analysis before the application is approved.

The above preparation by a professional should not be considered onerous. A taxpayer and all entities should have a financial plan in place. After all, this is just rudimentary financial forethought. The adage is “failing to plan is a plan for failure.”

On your projections, be as accurate as possible even if you must present best- and worst-case scenarios. For if the IRS accepts the taxpayer’s OIC, the IRS expects that the taxpayer will have no further delinquencies and will fully comply with the tax laws. If the taxpayer doesn’t fulfill their obligations by the terms and conditions of the OIC, the IRS could classify the OIC as in default. Recall that for the accepted OIC, the terms and conditions generally include a requirement that the taxpayer timely file all tax returns and timely payments of all taxes for 5 years. When an OIC is declared to be in default, the agreement is no longer in effect and the IRS may then collect the amounts originally owed (less payments made), plus interest and penalties.

In summary, ensure that the projections are achievable, and that the taxpayer can fulfill their obligations. If an unforeseen material issue arises, notify the IRS and have a plan on how the taxpayer is going to mitigate this exposure. Again, as stated above, no surprises to the IRS.

Business Valuation

This stage of the OIC process – the Business Valuation - is the “Achilles Heel” for most non-individual applications for the OIC. Recall, the OIC financial basis is driven by the ability to pay in the future (Projections) and the current economic environment (a Business Valuation). The IRS has not only defined the requisite requirements of an IRS valuator, but the IRS is most specific on the methodology and processes germane to business valuations to be submitted to the IRS.

A business valuation is a complex process, especially when addressing atypical business environments — distressed entities and the IRS. The IRS requires that the business valuator be a “Qualified Appraiser.” The regulations state a “Qualified Appraiser” is one who has earned an appraisal designation from a professional appraisal organization, has the appropriate education and experience, and performs appraisals on a regular basis.

Since 1959, the IRS (IRS Revenue Ruling 59-60) has created the expectations for its valuation requirements. In summary these being:

The nature of the business and its history

The book value of the company stock and its financial condition

The dividend paying ability of the firm

The presence of goodwill and other intangible assets

Sales of company stock, sizes of stock blocks to be valued

Market price of stock of companies in the same line of business whose stock trades freely on the open market

The tax authorities are typically interested in the business cash flow outlook. So, a realistic earnings forecast is useful both for your income-based business valuation as well as meeting the level of transparency expected of a well thought out business appraisal. However, as described below this is easier said than done.

Why is the Business Valuation so much more Complex for the OIC?

Attestation. The IRS requires that the valuation be formally certified by the business valuator. Furthermore, the business valuator for the IRS engagements must state that their opinion is not based to limit one’s tax payment but is a true reflection of the value of the business. Any offense to this certification carries severe professional penalties and liabilities. There are many business valuation firms that do not work with the IRS requirements due to this risk plus those listed below.

In addition, although all business valuations require proper document and supporting documentation, generally, the business valuations for the IRS are at the extreme end of the spectrum as it relates to documentation and supporting documentation. As you are aware, the burden of proof is on the taxpayer and the taxpayer is requesting a significant restructuring of a debt that is owed.

Going Concern. This is the #1 challenge associated with a business valuation associated with an entity that has significant tax obligations. In non-accounting terms: can this entity survive in the long-term given the overall obligations in comparison to its ability to pay? By definition of the OIC the entity’s unable to address its financial/tax obligations, when there is a significant likelihood that an entity will not survive the immediate future (next few years), traditional valuation models may yield an over-optimistic estimate of value.

Valuation Methodologies. Generally, a business valuation weighs three methods of valuing the entity:

Market Base – what is the value of their competitors in the market?

However, with the tax obligation outstanding and its inability to pay, this

does not allow for a meaningful valuation comparison to their competitors

Income Method (commonly referred to as the Discounted Cash Flow) – this

approach measures how much net income can be generated over the long-

term life of the entity at a discounted rate based upon risks. This method

also presents its own challenges with the OIC process. First, as described

above, does the entity have a long-term opportunity – is it a “going

concern?” Secondly, the risks associated with an entity in arrears to its tax

obligation plus its inability to pay such obligations yields an extremely

high-risk factor. This quantified risk factor can be so high that this income

method will not yield meaningful results

Asset Method – what are the value of the underlying assets of the entity

less its liabilities/obligations. Remember for the IRS purposes, generally -

the valuator can reduce the valuation by the tax obligation in full. For the

sake of simplicity, let us assume that we can determine all the assets both

tangible and intangible (including goodwill and Intellectual Properties).

The challenge in the asset method of valuating the assets in such an entity

are what premise does one value these assets?

Fair market value (FMV) is the price that property would sell for on

the open market. It is the price that would be agreed on between a

willing buyer and a willing seller, with neither being required to act,

and both having reasonable knowledge of the relevant facts.

The fair value as the “the price that would be received to sell an

asset or paid to transfer a liability in an orderly transaction between

market participants at the measurement date.”

The orderly liquidation value (“OLV”) is typically included in an

appraisal of hard tangible assets (i.e., equipment). It is an estimate

of the gross amount that the tangible assets would earn in an

auction-style liquidation with the seller needing to sell the assets on

an “as-is, where-is” basis.

Forced Liquidation Value (“FLV”) is the values expected to be

produced if the company or machinery and equipment had to be

disposed of much more quickly. For example – what if the assets

must be sold within 90 days. This would significantly diminish the

value of the assets in comparison to the OLV.

When selecting a Qualified Appraiser, ensure that the firm has significant experience in dealing with distressed or challenged entities. The core facts are so different and require a totally different set of parameters. Secondly, ensure that the Qualified Appraiser has had experience in being an expert witness so that they can explain their methodology, procedures and working papers.

Risk of the entity – The foundation of the business valuation is based upon the ability to generate revenue and its correlated risks. As briefly described above, the risks associated with materially outstanding tax obligations as it pertains to the entity’s survivability generates a risk (discounted rate) so high that the associated results are too often skewed to be beneficial or reflective of the true economic value of the entity.

The format and components required by the IRS in the OIC environment are atypical. Therefore, experience in dealing with distressed entities, understanding of the tax code, ability to communicate the results as an expert witness and knowledge of the business valuation methodologies are prerequisites that a Qualified Appraisers needs to assist you, the tax professional, in optimizing your client’s chances of obtaining the OIC.

Mythic of the OIC Amounts

Although the IRS has numerous guidelines on how to determine the OIC amount if accepted, there are no “fast and set” calculations to derive the OIC amounts and/or payment schedules. There is no doubt that the criteria is based upon the ability to pay in the future (projections) + the valuation of the net assets. But it is the combination of the aforementioned factors that determine the amounts involved.

The reality is success with an OIC is based on a full understanding of the IRS investigative process into ability to pay coupled with the net value of the assets in question. It is not a one size fits all situation; the amount of one person’s settlement has no bearing on the success of another’s. The IRS does not have a set percentage of settlement to the amount owed.

An Offer in Compromise does not affect your credit. Credit services have no idea that you have filed an offer or are seeking relief. The key is that your offer is accepted. Once the offer is accepted and paid, any tax lien should be released.