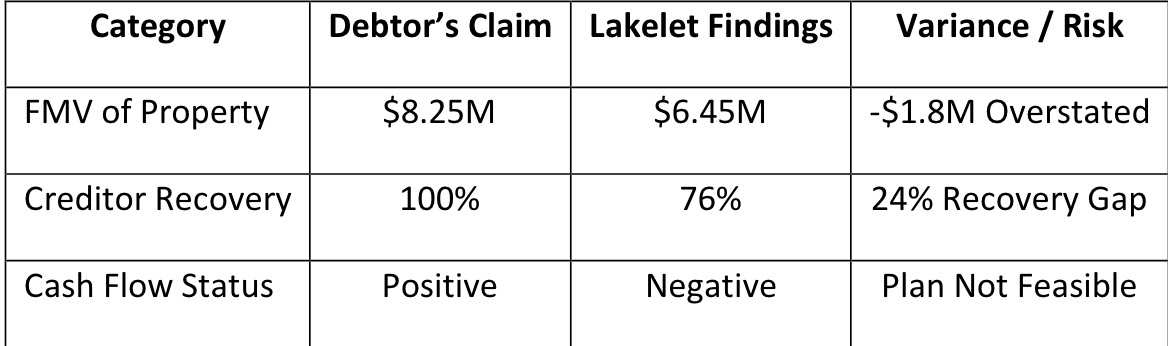

Background:

A debtor company filed for Chapter 11 bankruptcy, owing $486,000 to three Merchant Cash Advance (MCA) creditors. Each MCA was preparing to take separate independent actions against the debtor. This approach would have generated redundancies in costs. Lakelet Advisory Group LLC was able to persuade these three MCAs into collaborating with us to address the financial analysis, valuation of the debtor and assessment of the collectability of the unsecured debt.

Strategic Rationale for Consolidation:

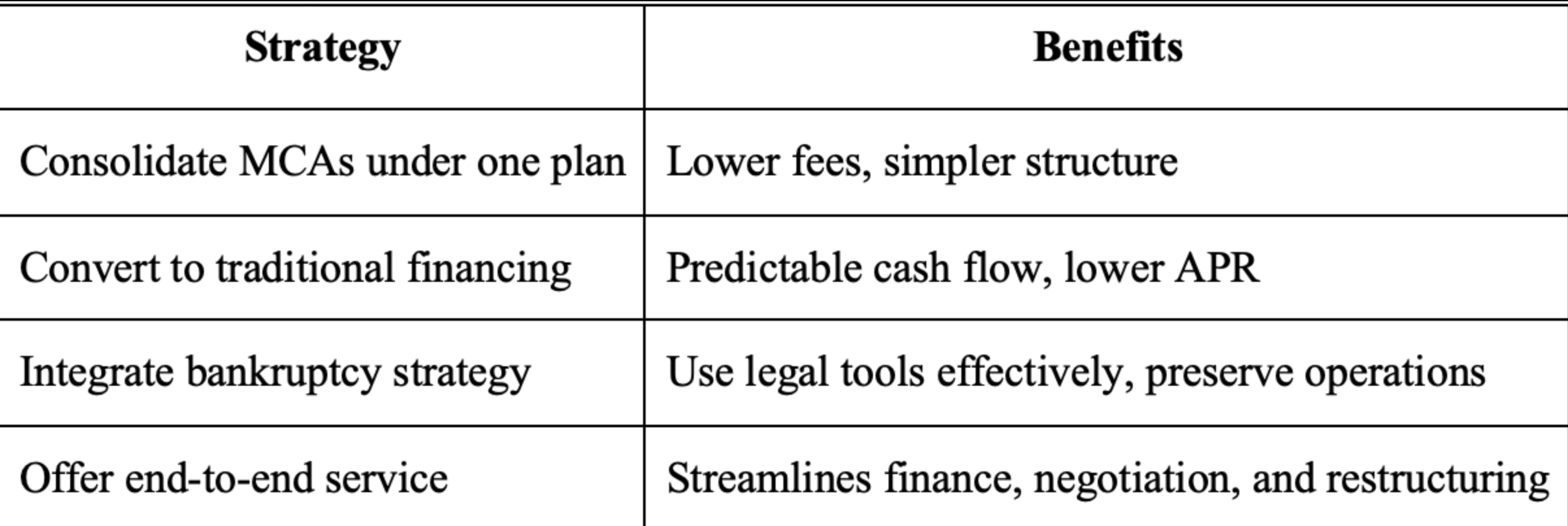

Lakelet Advisory Group LLC created a unified approach to help MCA creditors improve their recoveries, cut costs, and simplify the bankruptcy process.

A collective approach is best for MCA creditors because it offers stronger negotiating power by combining claims, resulting in better settlement terms. It also lowers legal and valuation costs through a single financial investigation. Additionally, it speeds up the resolution with cooperation among legal teams and experts, preventing delays. Finally, it optimizes recovery by aligning interests rather than competing for funds.

Solution: Coordinated Legal & Financial Forensic Strategy:

To eliminate inefficiencies and maximize recovery, the three MCAs pooled resources and engaged our firm for a unified financial forensics and business valuation analysis. Key components included a comprehensive business valuation to assess if the debtor’s assets exceeded liabilities and recovery potential. It also involved a financial forensics investigation to uncover insider payments before bankruptcy, strengthening clawback arguments. Additionally, a unified legal strategy ensured MCA creditors were aligned, preventing the debtor from pitting them against each other.

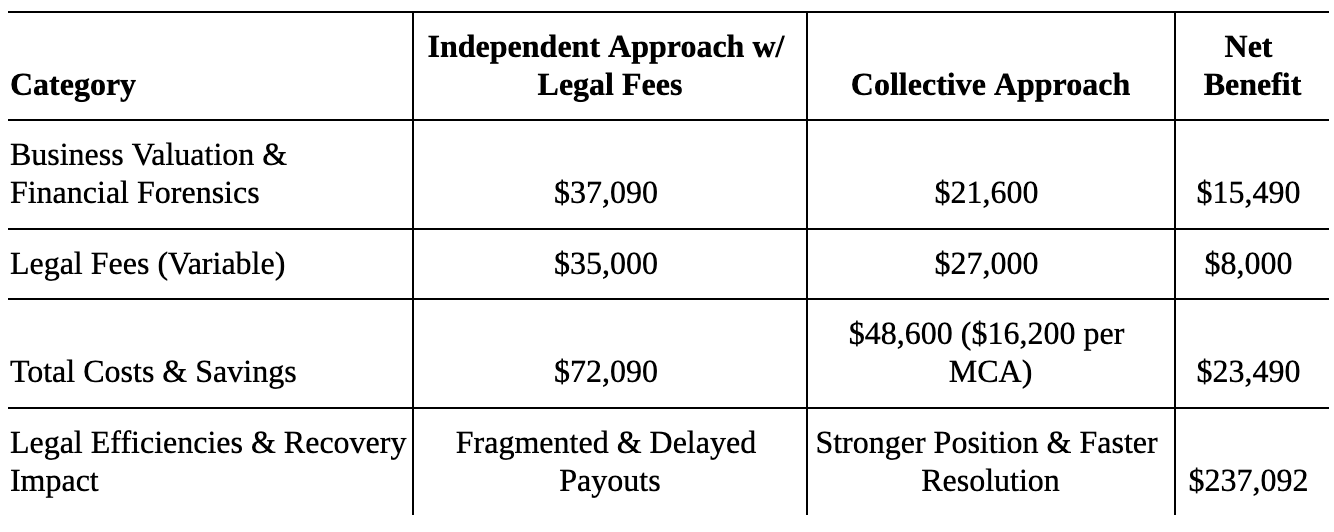

Financial Breakdown: Independent Costs vs. Collective Synergies:

Key Benefits of the Consolidated Approach & the Outcome:

Key Benefits of the Consolidated Approach include cost savings and shared expenses, where each MCA paid a fixed amount instead of excessive fees, saving $15,490 in financial forensics and business valuation. A unified legal approach strengthened the case in court and prevented delay tactics by the debtor. The approach also allowed faster claims processing and identified fraudulent transactions for higher recoveries. The outcome included net savings of $268,000, a stronger legal strategy, quicker bankruptcy resolution, and optimized collection per MCA.

Conclusion: Why MCA Creditors Should Consolidate Efforts in Bankruptcy Cases:

Introduction: This case shows the benefits of teamwork among MCA creditors.

Key Points:

Shared resources lower costs while maintaining quality.

Legal fees become more predictable.

The bankruptcy process is quicker, enhancing recovery.

Collaboration boosts overall recovery rather than competing.

In MCA bankruptcies, combining resources and strategies improves recovery and reduces costs for all involved.