While ESOP-owned companies and non-ESOP companies are generally valued under the same fair market value (FMV) standard, the resulting conclusions can differ materially due to structural, economic, and regulatory factors inherent to ESOP transactions.

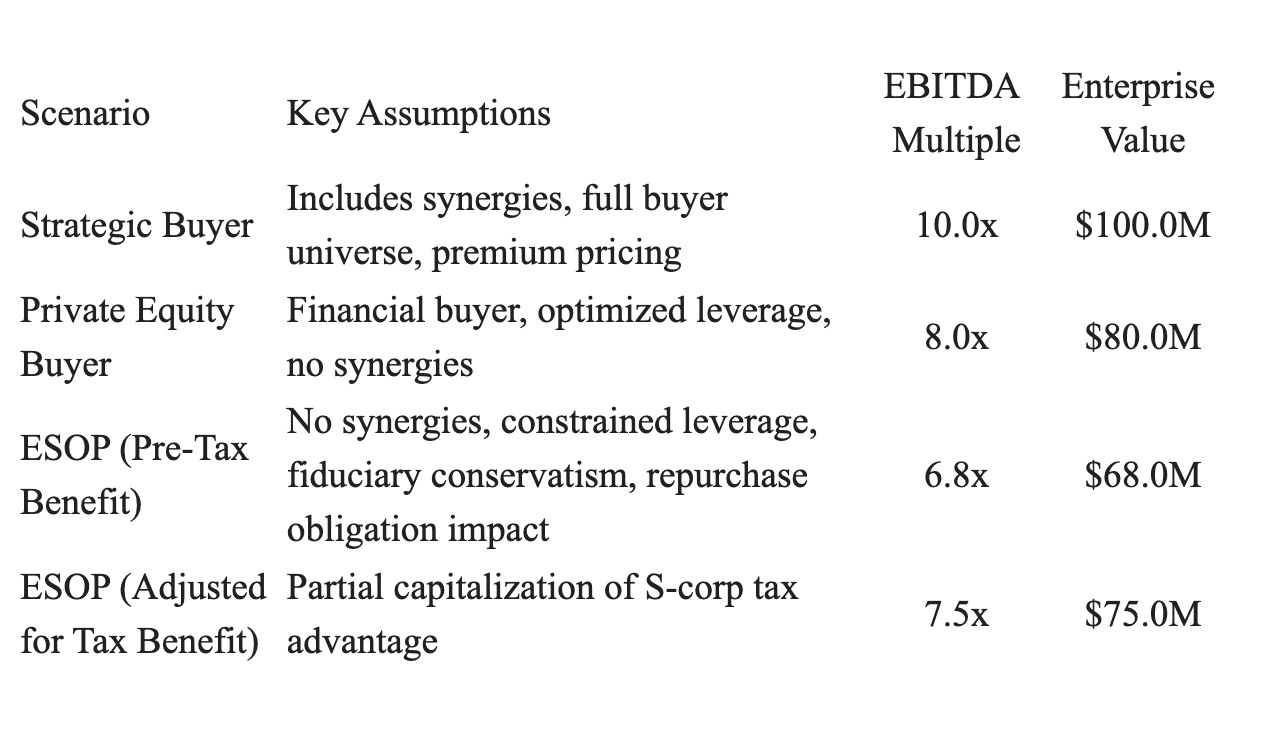

In a conventional valuation context, the hypothetical buyer universe includes both strategic acquirers and financial sponsors, and therefore implicitly reflects the highest and best use of the business. Strategic buyers, in particular, may incorporate expected synergies—such as cost savings, revenue enhancement, or market consolidation—which can support premium valuation multiples. Private equity buyers, while not paying for synergies to the same degree, often utilize optimized leverage structures to enhance returns, supporting competitive pricing.

In contrast, an ESOP transaction is fundamentally different. The buyer is not a market participant in the traditional sense, but rather a trust acting on behalf of employees, subject to ERISA fiduciary obligations. As such, the ESOP must pay no more than adequate consideration, interpreted as fair market value under a prudent and defensible process. This eliminates the influence of strategic synergies and constrains the valuation to what a financial buyer with limited leverage capacity can support.

Additionally, ESOP-owned companies introduce unique economic considerations that directly affect value. One of the most significant is the repurchase obligation, which requires the company to buy back shares from departing employees. This obligation functions as a long-term cash flow claim, effectively reducing the free cash flow available to service debt or distribute value, and therefore placing downward pressure on valuation.

Conversely, ESOP structures—particularly S-corporation ESOPs—benefit from a substantial tax advantage, as the ESOP-owned portion of the company is generally exempt from federal income tax. This increases after-tax cash flow and, in theory, enhances value. However, in practice, this benefit is often only partially capitalized in valuation due to fiduciary conservatism and ongoing regulatory scrutiny.

Further differences arise in the treatment of control and marketability. Although ESOPs frequently acquire controlling interests, the absence of a liquid external market for shares necessitates consideration of a discount for lack of marketability (DLOM). At the same time, any control premium must be carefully justified and is often tempered or offset by the lack of liquidity.

Finally, ESOP valuations are influenced by a heightened emphasis on defensibility. Given the potential for Department of Labor (DOL) review and litigation, valuation assumptions—such as projections, discount rates, and terminal values—tend to be more conservative, further contributing to differences in outcome relative to a typical market-based valuation.

Taken together, these factors generally result in ESOP valuations that are lower than strategic transaction values and often comparable to or modestly below private equity valuations, depending on the specific facts and circumstances.

Illustrative Valuation Comparison

Assumptions:

EBITDA: $10.0 million

Identical underlying business across scenarios

Summary Insight

The divergence in valuation outcomes is best understood as a function of buyer-specific constraints and structural economics, rather than differences in underlying business performance.

In effect, a traditional valuation reflects what the business could command in a competitive market, whereas an ESOP valuation reflects what a fiduciary-bound, financially constrained buyer can prudently pay, given regulatory obligations and long-term sustainability considerations.