A fintech platform reported default rates of 8.5% to 10.5% among MCA borrowers. This gives us a rough idea of accounts that go into default. As a benchmark, traditional business loan delinquency stands much lower—at 1.16%.

A small to mid-size entity in bankruptcy averages ~3 MCAs per filing.

Lakelet Advisory Group’s Service for MCAs.

Lakelet Advisory Group helps MCA providers protect and maximize recovery in distressed situations. We analyze contracts for recharacterization risks, usury exposure, and UCC perfection to strengthen legal standing. Our forensic team traces receivable flows, identifies preference or fraudulent transfers, and models expected recovery under Chapter 7 or Chapter 11. In litigation, we support counsel with expert testimony, financial exhibits, and loss quantification, while also developing workout strategies that preserve cash flow outside of bankruptcy.

Beyond individual cases, we conduct portfolio risk reviews, highlight exposure to stacking and industry concentrations, and provide regulatory insights shaping MCA enforceability. With deep experience in valuation, bankruptcy, and financial forensics, Lakelet Advisory Group delivers clarity, defensibility, and actionable strategies—helping MCA providers improve collectibility and mitigate risk.

Legal Characterization and Direction of MCAs

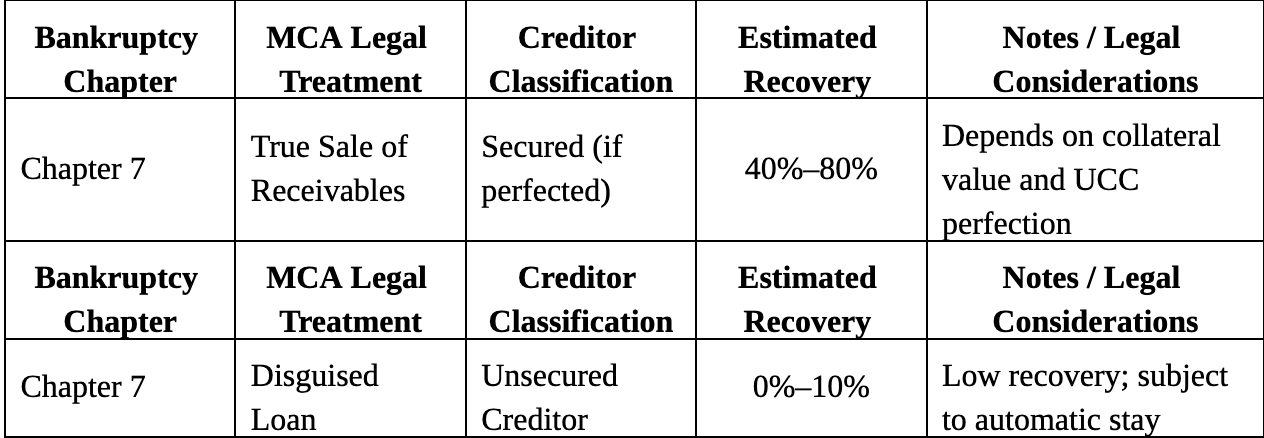

The legal treatment of MCAs in bankruptcy depends on whether the transaction is deemed a “true sale” of receivables or a disguised loan. Courts examine the substance over form, with key factors including:

· Whether repayment is contingent on actual receivables

· The presence of a fixed repayment schedule

· Recourse against the merchant if sales decline

· The use of personal guarantees and confessions of judgment (COJs)

If classified as a true sale and secured with a perfected UCC filing, the MCA provider may recover directly from receivables and avoid inclusion in the bankruptcy estate under §541 of the Bankruptcy Code. However, in most cases, courts have found MCA agreements to be loans, rendering them unsecured claims subject to the automatic stay under §362 and substantially reducing recovery prospects. Additionally, aggressive pre-petition collections can be clawed back as preferences (§547) or fraudulent transfers (§548).

Market Trends, Regulatory Actions, and Case Outcomes

Market Scale & Growth: Published market-size estimates diverge, but all show rapid growth. Allied Market Research pegs 2023 global MCA volume at $17.9B with a forecast to $32.7B by 2032 (CAGR ~7.2%).[1] Some trackers report even steeper trajectories, but methodologies vary.[2]

Bankruptcy courts are increasingly scrutinizing “true sale” claims. Recent S.D.N.Y. rulings (e.g., In re J.P.R. Mechanical, Inc.) recharacterized MCA agreements as loans and allowed the clawback of >$3M in pre-petition payments, despite “sale of receivables” labels, highlighting preference exposure when reconciliation is weak or term/recourse looks loan-like.[3]

Small-business demand context. Federal Reserve Small Business Credit Survey shows firms’ applications for loans/LOCs/MCAs dipped from 40% to 37% (2022→2023), with approval rates largely unchanged owners continue turning to non-bank options when banks tighten.[4]

There is no widely published data on the average number of MCAs per bankruptcy, but “most small business debtors under Subchapter V of Chapter 11 have at least one merchant cash advance creditor.”[5] For businesses filing for Chapter 11 to have more MCA obligations stacked on top of each other, especially when financing, has become a repeated, urgent solution.

MCA Recovery Outcomes by Bankruptcy Chapter and Legal Classification

In distressed scenarios or bankruptcy, MCA providers often experience sharply negative returns. For example, on a $100,000 advance with a contractual repayment of $135,000, a 10% recovery over 12 months equates to a -90% ROI. Breakeven occurs only with full recovery of the advanced amount, not including profit. Typical distressed recoveries for recharacterized MCAs are under 20%, especially in Chapter 7 liquidations.

Why This Matters to Recovery Outcomes

If an MCA is recharacterized as a loan in bankruptcy, the claim is typically unsecured, subject to the automatic stay, and prior collections can be avoided as preferences or fraudulent transfers, slashing recoveries vs. “true sale” treatment with perfected security interests. Enforcement actions and COJ limits increase the odds that aggressive pre-petition debits are challenged and clawed back, or that contractual terms are voided, directly affecting net ROI.[6]

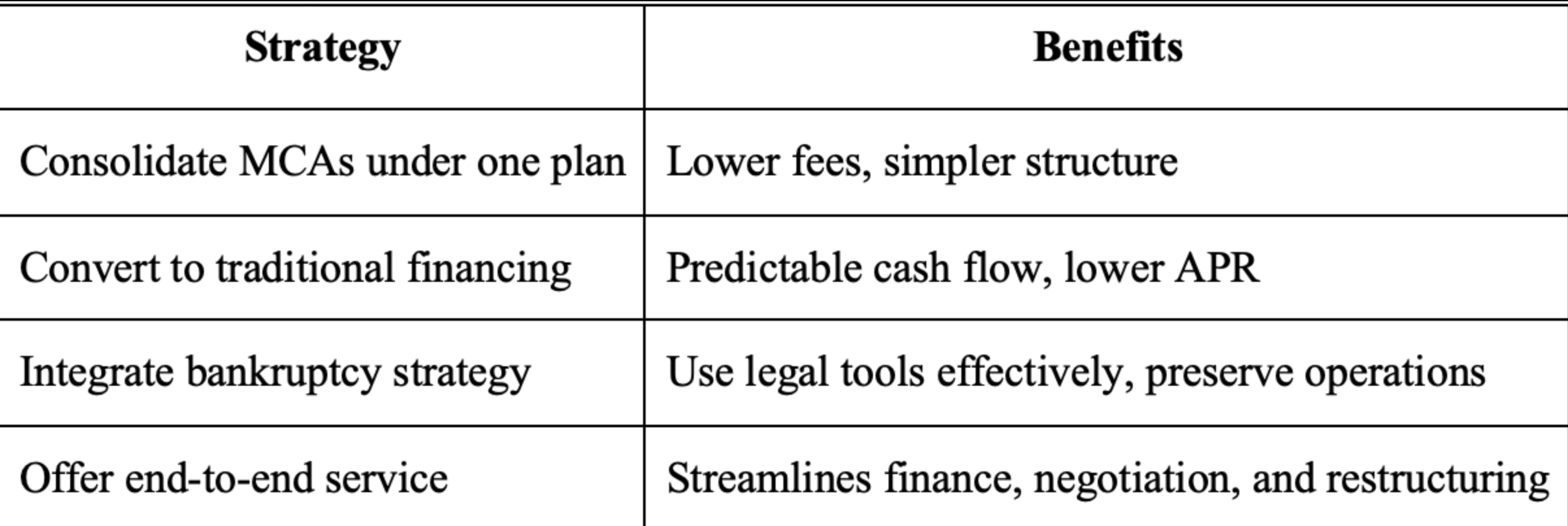

Adding Value by Consolidating Services

If your firm can consolidate services and address MCAs strategically, you can offer distinct advantages:

1. Cost Reduction

· Simplify servicing: Consolidating MCAs into a single structured arrangement (e.g., a term loan or manageable repayment plan) can lower administrative overhead and eliminate the high factor fees—typically 1.1× to 1.5× the advance.[7]

· Reduce expensive stacking: Prevent businesses from entering repeated MCA cycles that dramatically increase costs via repetitive high repayments.[8]

2. Risk Mitigation

· Improved cash flow predictability: Replacing daily or weekly holdbacks with structured repayments reduces volatility and helps clients budget more effectively.[9]

· Avoid legal pitfalls: MCAs often come with aggressive terms like ACH withdrawals, personal guarantees, and UCC filings. Consolidation into more standard, transparent terms lowers exposure to defaults and potential litigation.[10]

3. Enhanced Negotiating Leverage

· In bankruptcy contexts, you can use tools like automatic stay, prioritizing claims, or negotiating secured vs unsecured status to streamline resolution. Consolidation supports such strategic maneuvering.[11]

· Professional representation: Your integrated services (valuation, restructuring, negotiation) give the client a stronger, more credible position with MCA funders and the court.

Lakelet Advisory Group: Litigation Support That Moves the Needle

Lakelet Advisory Group helps determine what’s collectible, what’s avoidable, and what’s negotiable in MCA disputes. Here’s how we add value (and why it benefits your case):

Deal Characterization & UCC Perfection Review: We test MCA terms against the three core factors courts scrutinize (contingency on receivables, fixed terms, and recourse) and verify perfection gaps to argue secured “true sale” when supportable or to pressure concessions when it isn’t. This can shift a claim from unsecured to secured (or vice versa), materially changing expected recoveries.

Preference/Fraudulent-Transfer Analytics: We reconstruct payment flows and timing to quantify §547/§548 exposure; critical when rulings like J.P.R. Mechanical show millions can be clawed back. Quantifying that exposure tightens settlement ranges and informs plan negotiations.[12]

Forensic Receivables Tracing: We map pre- and post-petition receivable streams, identify carve-outs, and surface third-party payment processors or lockbox gaps, creating actionable leads for turnover demands or adequate-protection negotiations.

Expert Support & Testimony: We translate industry mechanics (reconciliation practices, factor rates vs. APR optics, COJ usage) for the court, aligning with evolving case law to strengthen usury defenses (when appropriate) or to support recharacterization arguments.[13]

Plan & Workout Modeling: We build scenario models (sale vs. loan characterization; secured vs. unsecured; preference outcomes) to set settlement anchors and accelerate resolution, improving time-to-cash vs. protracted litigation.

The MCA industry remains a fast-growing alternative finance sector, but legal recharacterization risks in bankruptcy substantially impact recoveries. At Lakelet Advisory Group, we provide effective litigation support and proactive restructuring to ensure true sale status and perfected security interests. We have a proven track record of materially improving collection prospects.

[1] Allied Market Research. Merchant Cash Advance Market. https://www.alliedmarketresearch.com/merchant-cash-advance-market-A323338

[2] Global Growth Insights. Merchant Cash Advance Market Report. https://www.globalgrowthinsights.com/market-reports/merchant-cash-advance-market-102198

[3] Eversheds Sutherland. Preference Pitfalls for Merchant Cash Advances: Lessons from the Southern District of New York. https://www.eversheds-sutherland.com/en/global/insights/preference-pitfalls-for-merchant-cash-advances-lessons-from-the-southern-district-of-new-york

[4] Federal Reserve Banks. (2024). 2024 Report on Employer Firms: Findings from the 2023 Small Business Credit Survey. https://doi.org/10.55350/sbcs-20240307

[5] McConville Considine Cooman & Morin, P.C. The Dangers of a Merchant Cash Advance. https://www.mccmlaw.com/news-and-articles/articles/the-dangers-of-a-merchant-cash-advance

[6] Federal Trade Commission. Court Enters $203 Million Judgment in FTC Case Against Merchant Cash Advance Operator Jonathan Braun. https://www.ftc.gov/news-events/news/press-releases/2024/02/court-enters-203-million-judgment-ftc-case-against-merchant-cash-advance-operator-jonathan-braun

[7] Attorney-NewYork.com. Can You File Bankruptcy on a Merchant Cash Advance?. https://attorney-newyork.com/mca-debt/merchant-cash-advance-can-you-file-bankruptcy

[8] New Frontier Funding. How to Get Out of MCA Loans: A Comprehensive Guide. https://newfrontierfunding.com/how-to-get-out-of-mca-loans

[9] Rho Editorial Team. What is an MCA? Merchant Cash Advances for Startups. Rho (May 27, 2025). https://www.rho.co/blog/merchant-cash-advances-mca

[10] United States Bankruptcy Court, Northern District of Florida. Merchant Cash Advance Claims in Bankruptcy (by Caitlyn Coates & Michael Markham), April 2025. https://www.flnb.uscourts.gov/sites/flnb/files/2025-04_NSL_Guest_MerchantCashAdvance.pdf

[11] Coates, Caitlyn & Markham, Michael. Merchant Cash Advance Claims in Bankruptcy. United States Bankruptcy Court, Northern District of Florida (April 2025). https://www.flnb.uscourts.gov/sites/flnb/files/2025-04_NSL_Guest_MerchantCashAdvance.pdf

[12] Allied Market Research. Merchant Cash Advance Market. https://www.alliedmarketresearch.com/merchant-cash-advance-market-A323338

[13] New York Courts. Principis Capital, LLC v. I Do, Inc. 160 A.D.3d 501 (2018). https://www.nycourts.gov/REPORTER/3dseries/2018/2018_01645.htm