Assessing the value of a start-up is a crucial task that combines creativity with analysis. Unlike established companies, start-ups lack financial performance history and operate in competitive and fluid markets. The Going Concern principle must be considered in valuation, as most start-ups struggle to survive beyond their first decade[1]. Valuation methods like market comparisons, discounted cash flow (DCF), and earnings multiples can be challenging due to numerous factors.

The percentage of startups that successfully reach an Initial Public Offering (IPO) is quite low. Generally, only about 1% of startups ever reach the IPO stage. Most startups either fail, get acquired by larger companies, or remain private businesses.

It is important to grasp the business model, market trends, and competition before beginning the valuation process. This foundational knowledge shapes the assumptions that guide the valuation. This article presents an overview of the methodologies employed in assessing the value of a start-up, highlighting essential valuation techniques, necessary risk adjustments, the evaluation of intangible assets, and the critical role of confirming the accuracy of the outcomes.

Step 1: Understand the Business and Market

A start-up’s success is heavily dependent on its business model, which includes revenue sources, cost structures, and growth potential. It is essential to understand how the start-up provides value to customers, differentiates itself from competitors, and generates revenue using models like subscriptions or direct sales. Analyzing costs, scalability, and profitability is crucial for future success.

Market analysis is also vital, focusing on market size, growth trends, and competition. Evaluating the Total Addressable Market (TAM) and competitive landscape helps in identifying growth opportunities and potential market share.

Therefore, start-ups need to carefully analyze their business model, market dynamics, and internal and external factors to position themselves for success in the competitive business landscape. The ability to innovate, adapt, and leverage opportunities while mitigating threats will be essential for long-term sustainability and growth.

Step 2: Select an Appropriate Valuation Method

Valuing a start-up involves using various techniques to assess its potential and risks. Common methods include Discounted Cash Flow (DCF) analysis, Comparable Company Analysis (Market Approach), Venture Capital (VC) Method, Scorecard Method, Berkus Method, and Real Options Valuation (ROV). These methods help in estimating the start-up’s value by considering factors like revenue forecasting, expense forecasting, discount rates, and terminal value. Each method has key considerations and steps to follow for an accurate valuation.

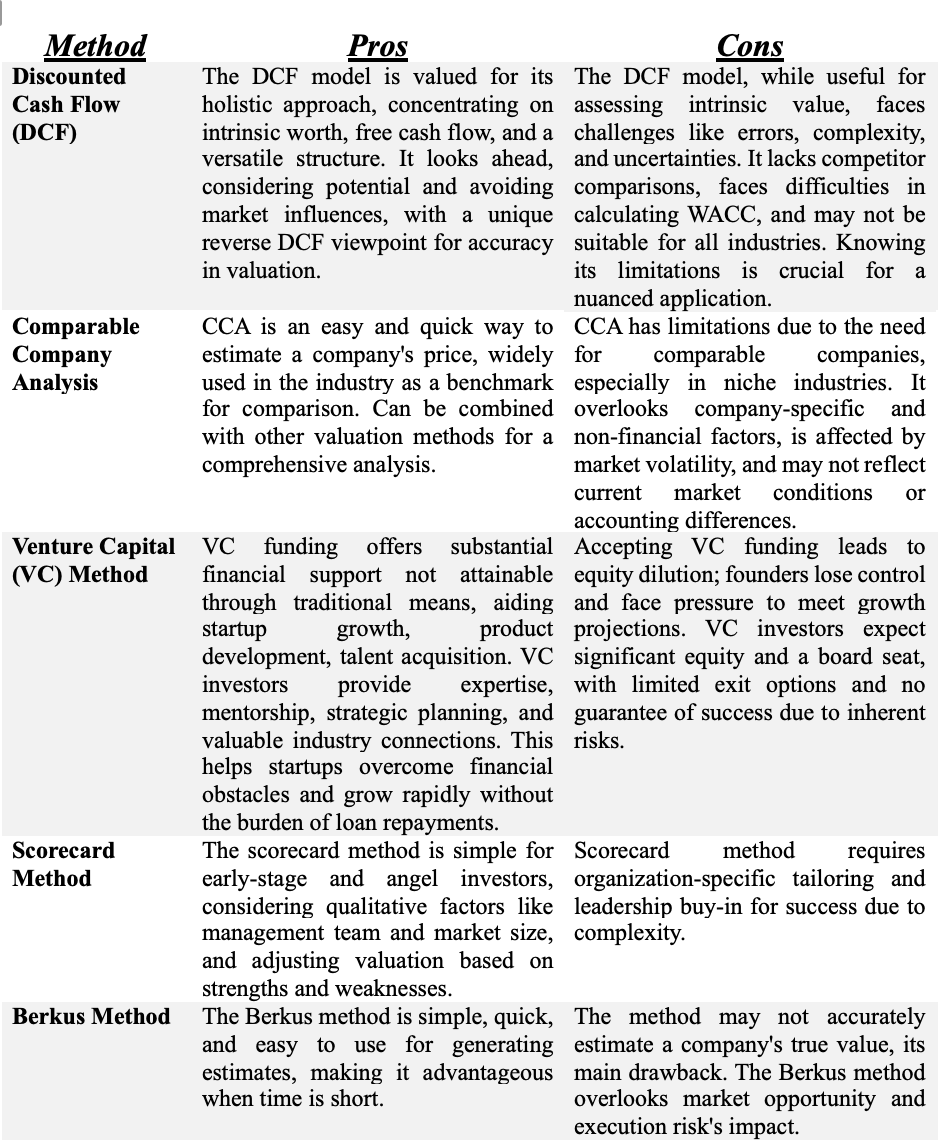

The Discounted Cash Flow (DCF) method involves estimating a start-up’s future cash flows and discounting them to present value using a discount rate. This method is ideal for start-ups with revenue and the ability to forecast cash flows. However, start-ups face higher risks, requiring elevated discount rates due to uncertainties in future cash flows and potential business failure. It is recommended to conduct scenario evaluations to assess different scenarios and provide a range of valuations based on various assumptions.

Or:

(DCF) = [FCF1 / (1 + r)1] + [FCF2 / (1 + r)2] + .... + [FCFn / (1 + r)n] + [FCFn × (1 + g) / (r - g)]

FCF = free cash flow

r = discount rate (required rate of return)

g = growth rate

n = time period

The Comparable Company Analysis, also known as the market approach, values a start-up by comparing it to similar publicly listed or recently acquired firms. This method is useful when there are limited financial projections or when the start-up operates in a well-defined industry with established competitors. Selecting appropriate comparable and adjusting valuation ratios based on growth rates, profit margins, and risk profiles are critical for an accurate valuation.

The Venture Capital (VC) Method is commonly used by investors to evaluate early-stage start-ups by predicting the future exit value through acquisition or IPO and discounting it to present using a high discount rate. This method demands high returns from investors due to the risk in start-up investments. Having a clear path to an exit event is crucial, emphasizing the importance of a well-defined exit strategy aligned with industry trends and investor expectations.

Exit Value / Post-money Valuation = Expected Return on Investment (RoI), or

Exit Value / Expected Return on Investment = Post-money Valuation (RoI)

The Scorecard Method compares a start-up against peers using specific criteria to determine its relative value in the market. Key criteria include management team quality, market size, product differentiation, competition, and financial projections. Assigning weights to each criterion, scoring the start-up, and adjusting average valuations based on scores help in estimating the start-up’s value.

The steps for using the scorecard method are:

Identify the baseline valuation: Determine the average pre-money valuation of similar companies in the same industry and region

2. Assign weights to key factors: Assign subjective ranges to factors, such as management team strength, product and technology, and competitive environment

Score and multiply: Compare the target startup to the average, and score each factor

Calculate the adjustment factor: Add all the multipliers to get the total adjustment factor

The Berkus Method assigns monetary values to key success factors in early-stage start-ups to determine their valuation beyond financial performance. This method focuses on intangible factors and is useful for start-ups with high intangible value. However, it may not fully consider financial performance, serving as both an advantage and a limitation.

The Berkus Method is a valuation method for pre-revenue startups that doesn’t use a cash flow formula. Instead, it assigns dollar amounts to five key success metrics to approximate a startup’s valuation:

Sound idea: The strength and feasibility of the startup’s core concept

Prototype: The value of a working prototype

Quality management team: The importance of an experienced leadership team

Strategic relationships: The value of established partnerships and relationships

The Real Options Valuation (ROV) method assesses a start-up’s flexibility and strategic choices like changing business models or expanding into new markets. This method is beneficial for start-ups facing uncertainty and strategic changes, capturing the value of future opportunities not seen in traditional methods. Conducting financial modeling to determine option values and adding them to the start-up’s base valuation helps reflect its growth potential and flexibility.

In conclusion, various valuation methods are available to assess the worth of start-ups, each with its own set of considerations and steps to follow. By utilizing these techniques, investors and stakeholders can make informed decisions regarding potential investments in start-ups and ensure alignment with risk tolerance and return expectations.

Calculate the Option Value: Implement a mathematical option-pricing model to calculate the value of the Real Option. Real Options valuation often utilizes the Black-Scholes model or the binomial options pricing model. These models essentially use a risk-adjusted discount rate for valuation.

The Black–Scholes (BSOP) model uses five variables to calculate the value of real options based on cash flow:

S: The underlying asset’s present price or stock price

E: The strike or exercise price

R: The risk-free interest rate for the option’s life

σ2: The variance, or risk measurement, of the underlying asset’s return

t: The time until the option expires

The BSOP model also uses the cumulative normal probability values of d1 and d2, represented as N(d1) and N(d2). The formulas for d1 and d2 are:

d1 = ln (S / E) + [R + (1 / 2) σ2] t / σ t

d2 = d1 − σ t

Step 3: Adjust for Risk and Uncertainty

Start-ups are inherently risky, so it is crucial to adjust their valuations accordingly. One way to do this is by using high discount rates in methods like DCF and VC to factor in the uncertainties associated with start-ups. Market risk, business risk, and execution risk should be considered when determining these rates. Scenario analysis is also helpful, as it allows for the assessment of various outcomes like best, worst, and base case scenarios. This helps in understanding the range of possible values and associated risks. For a more advanced analysis, Monte Carlo simulations can be used to model different outcomes and their probabilities, providing a nuanced view of valuation under uncertainty. Key variables like revenue growth and exit multiples should be identified, and simulations should be run to generate possible outcomes. Analyzing the results can help understand the distribution of valuations and identify key drivers of uncertainty. Ultimately, adjusting for risk in start-up valuations involves considering several factors and using tools like scenario analysis and Monte Carlo simulations to make informed decisions.

Step 4: Consider Intangible Assets

Intangible assets play a crucial role in the value of start-ups, especially in technology-driven or IP-focused sectors. Consider the following intangible assets when assessing a start-up: Intellectual Property (IP), including patents and trademarks; Brand Value, which includes brand recognition and customer loyalty; and Customer Base and Contracts, which offer revenue stability. When valuing a start-up, factors to consider are Patent Valuation, Trademarks and Branding impact, Proprietary Technology value, Brand Equity strength, Market Positioning advantage, Customer Lifetime Value calculation, and Recurring Revenue streams. Evaluating these factors can help determine the overall worth of a start-up and its potential for future growth. Intangible assets are essential for creating a competitive edge and generating stable revenue streams, which are vital for reducing risk and ensuring long-term success.

Step 5: Validate and Cross-Check

It is important to verify and confirm the valuation of a start-up using various methods and viewpoints to ensure accuracy. By triangulating results from different valuation techniques, discrepancies can be identified and analyzed by examining the underlying assumptions. Consistency checks should be conducted to ensure alignment between results and assumptions about the start-up’s future growth and market conditions. Adjustments may be necessary if there are significant differences, such as revisiting revenue projections or discount rates. Comparing the valuation to industry benchmarks and seeking feedback from experts in the same field can help refine the valuation process and ensure it aligns with market expectations.

Conclusion:

Valuing a start-up is complex and requires careful consideration of several factors. By following a structured process, it is possible to arrive at a valuation that reflects the start-up’s potential and risks. Whether you are an entrepreneur seeking investment, an investor evaluating opportunities, or a financial analyst providing valuation services, mastering this process is essential for informed decision-making.

This guide offers practical advice and insights into valuing start-ups. By following these steps, you can improve the accuracy and credibility of your valuations, contributing to the success and growth of the start-up ecosystem.

About Lakelet Advisory Group:

Lakelet Advisory Group is a leading independent consulting firm that provides complex business valuations, business optimization and turnaround and restructuring services. Our highly credentialed experts focus like a laser on delivering tangible results to our clients. Lakelet Advisory Group has a proven track record by leveraging our comprehensive services and global experience.